Why Logic Drives Probability Teck Activates Copaquire Royalty

"Australian-UK resources group BHP estimates that declining grades will remove around 2mn t/yr of global copper mine supply by 2030, with resource depletion potentially removing an additional 1.5mn-2.25mn t/yr by that time." [1]

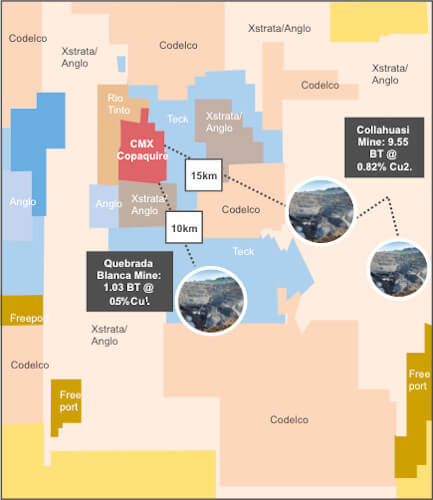

The impending copper shortage will make deposits like Copaquire attractive for development. Copaquire was discovered by Power Nickel (previously called Chilean Metals) and is now owned by Teck Resources.

Power Nickel sold its Copaquire property to Teck Resources Limited for Cad. $3,033,500, with CMX retaining a 3% NSR (net smelter return) royalty on production. Teck has the right to purchase one third of the NSR for Cad. $3,000,000, thereby presenting the Company with near-term cash flow potential. By way of comparison, total sales in 2013 at Quebrada Blanca, Teck’s nearby copper mine and SXEW operation, were $422 Million. The royalty, whether 3% or reduced to 2% through Teck exercising its right, has potential to provide significant future benefit to the Company in terms of non-dilutive exploration funding and/or dividends to our shareholders, and may provide a model for the Company’s future accretive growth.

Copaquire is located in Chile’s 1st Region, 125 kms south of its capital city, Iquique, on upland plateau in a very well-endowed mineral neighbourhood and readily accessible via well-maintained all-weather roads. The project adjoins Teck’s Quebrada Blanca mine, where leachable copper reserves will be depleted by 2016 at current production and reserve levels (Teck website). Anglo-Xstrata-Mitsui’s colossal Collahuasi copper mine also lies nearby.

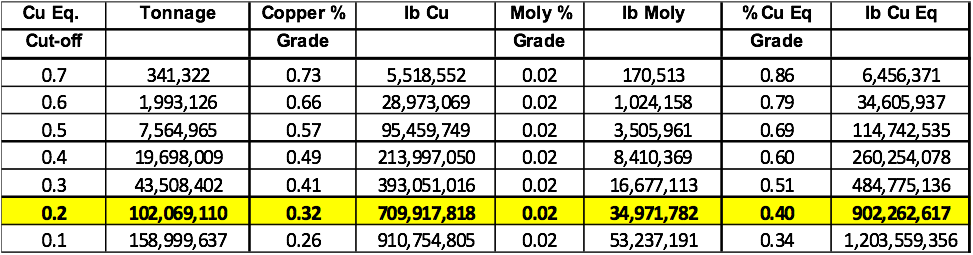

Copaquire boasts two 43-101-compliant resources: Sulfato South (dominantly copper) and Cerro Moly (dominantly molybdenum). Resources at the two deposits are listed in the following tables:

Sulfato South inferred mineral resource:

* Inferred mineral resource estimate by copper equivalent cut-off grades. These results are reported in metal equivalent data based on US $2.50/lb copper and US $13.50/lb molybdenum. In calculating copper equivalencies 100% metal recoevries have been assumed. Source: Charchafile, Jaramillo NI 43-101 Jan 30 2012.

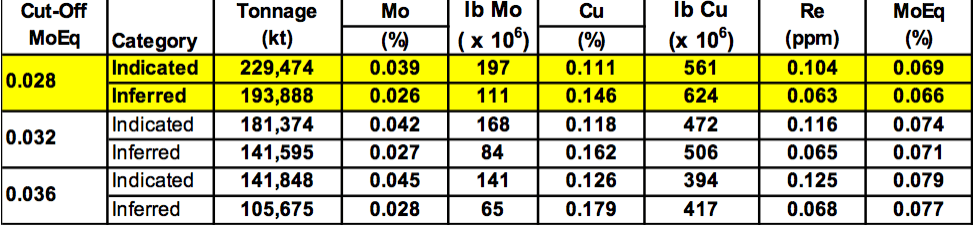

Cerro Moly indicated and inferred resources:

* Molybdenum equivalent (MoEq) grades are calculated using the following formula: MoEq(%) = Mo(%) + 1.35 * (Cu(%) * 2.3 / (Mo(%) * 12.65 - 1.14)). This formula assumes a selling cost of US $1.14/lb for Mo and metallurgical recoveries of 84% for Cu and 62% for Mo. Source: Videla, 2009, corroborated by AMEC (2009) NI 43-101. AMEC calculated a waste to ore strip ratio of 0.52/1 for the highlighted base case.

There exists significant potential to define a mineable secondary enrichment copper resource at Sulfato South. The secondary zone or blanket, estimated at up to 100 metres thick in previous drill holes, was not separated from the general Sulfato resource in the above resource calculation. In-fill and step-out drilling is needed in this largely untested area. The secondary enrichment blanket is generally higher grade than the primary copper resource, closer to surface (hence lower stripping costs), and lends itself to more profitable heap leaching-SXEW processing.

We believe that the odds of Copaquire being developed by Teck in the medium term and hence triggering our royalty are excellent. Declining copper grades, as noted above, and the structural supply shortages have already positively moved copper markets and will likely continue to develop forward price curves that will ultimately drive the development of Copaquire.